It's no surprise, if you know me, that you know I love a bargain and love to learn tactics on being more financially savy! I get the bargain side from my mom who has taught me the tricks of shopping at Thrift Stores and checking out the sale section first, for the past 20 years! I get the financial 'savy-ness' from my dad, who's always been GREAT with money! And I get my love for budgeting from my diagnosed OCD... I like to think of it as a blessing! :) I came to Korea for the experience, not the money. But, I've been pleasantly surprised with the amount I've been able to save in the 4 years I've worked here! I've had a lot of friends and acquaintances ask me how I've saved so much and I've been debating for a long long time on whether I wanted to tackle the $$$ issue on my blog, but I've recently been able to help someone change their life with this stuff, so I decided it's time to speak up! So, here are the Jillers tricks on how to manage your $$$ while living in Korea and become a (₩)-millionaire while doing it! |  from: Jill's Other Side of the Moon from: Jill's Other Side of the Moon |

1. Stay another year, or two, or three!

There are amazing incentives to staying in Korea for more than 1 year if you work for EPIK. For example, you get an extra 4 million (₩) deposited into your bank account each time you renew! Here's 4,000,000 (₩) worth of 10,000 (₩) bills for a quick visual.

Kinda worth staying, right?

... Plus every year you stay in Korea, your pension adds up (if you're American)! When you leave Korea, you'll get the equivalent of 1 paycheck for each year that you've worked here. For instance, if you stay in Korea for 4 years and make 2.5 million a month, you'll leave here with 10 million (₩) from your pension ($9300) to add to your savings account! SCORE, right?!

---------------------------------------------------------------------------------------------------------------------

2. For married couples.

Live in 1 school's apartment together. The other person will qualify for the housing stipend of 400,000 (₩) per month from their school, which adds up to 4,800,000 (₩) a year, just by living in a smaller place together. Aaron and I are doing it that way and we're so happy we did! We can live in a bigger house when we move back to America if we want, but for now we'll enjoy our tight space in Asia and the extra $4,500 a year we're making by living in it.

3. Get yourself on a budget!

I can't stress this enough! Download and print this document that I made, and keep up with it. After a month you'll see where all your money is going! You might be surprised! I know Aaron was when he first asked me to help him save money 3 years ago! He was spending almost $100 on his morning coffee every month! That's $1200 a year on coffee! He started making coffee at home before work at a fraction of the cost! So, the way this budget works is, every time you spend money, you color in the bars. Each bar is 5,000 (₩), so if you spend 2,500 on something, only color in 1/2 of the bar. You can change the line items by downloading this file, editing it, then printing it.

---------------------------------------------------------------------------------------------------------------------

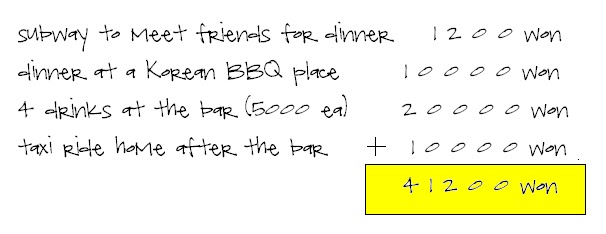

4. Stay in, cook dinner at home and watch a movie!

---------------------------------------------------------------------------------------------------------------------

5. Brew your coffee at home

I looooooove Vanilla Latte's at Starbucks, but if I bought one every morning on my way to work, I'd spend a pretty penny! You may be thinking, but Jill, I "need" my morning coffee! I agree with you, except you don't NEED Starbucks, Angel-in-us or Coffee Bean & Tea Leaf coffee! You could save hundreds of dollars by making it at home before you leave for work! Let's do the coffee math.

---------------------------------------------------------------------------------------------------------------------

6. Listen to Dave Ramsey Podcasts.

My parents definitely put me on track to be financially savvy at a young age... Dave Ramsey helped me, as I became an adult, to manage my money and pay off my student loans in a timely manner. Not to mention, he inspired me to be debt free, which I've been since I paid off $35,000 in student loans at 23! He may come across as really cocky at points, but his advice is right on the money and you'll walk away inspired to be debt free!

Click here to listen!

--------------------------------------------------------------------------------------------------------------

7. Avoid buying stuff at full price!

---------------------------------------------------------------------------------------------------------------------

8. Pay with cash in Korea.

---------------------------------------------------------------------------------------------------------------------

9. Buy online and use coupon codes!

I can't tell you how much I've saved by buying some of the things I need online! Korea can be cheap if you know where to shop, but buying online can be even cheaper! If you're in the market for electronics, jewelry, purses, foreign goods, shoes, clothes, etc... try some of these websites that I use! Most, if not ALL ship to Korea too.

www.gmarket.co.kr (for anything Korean)

www.ioffer.com (for purses, jewelry, clothes, etc)

www.iherb.com (for healthy foreign food, spices, all natural toiletries, etc)

www.ebay.com / www.ebay.co.uk (for EVERYTHING)

*** If you're shopping at any other store online, go to www.retailmenot.com before you check out, and type in the website's name where your buying something from. There will most likely be a coupon code to give you a discount on your order! I just found this coupon code for 25% off the H&M store on ebay! See what I mean?!

---------------------------------------------------------------------------------------------------------------------

10. Make it if you can!

This applies to everything from food, cleaning supplies, home decor, gifts, etc. I know not everyone out there is crafty or knows their way around a sewing machine, but if you do, start making stuff instead of buying it! I've made curtains for my apartment, about 10 pillow cases, a duvet cover, a bed skirt, picture matings, wall hangings, clothes, holiday banners and a bunch of other stuff, and saved myself hundreds of dollars! I borrowed a sewing machine from my school's 6th grade classroom. Your school might have one too that you can take home and use! It's worth asking, right?! I also make my own custom Christmas cards and did custom Christmas mugs this year too, which would be a great gift for co-workers! Aaron and I also cook healthy meals at home, almost every night, for between 3 - 5,000 (₩) a person! Sure beats going to Outback, TGIFridays or a Korean Beef restaurant and being handed a bill for 50,000 (₩)!

---------------------------------------------------------------------------------------------------------------------

11. Find a cheap hobby!

1. Try blogging, it's FREE!

2. Buy or check out a book from the English library and snuggle up with some homemade coffee.

3. Watch movies on www.documentaryheaven.com

4. Start a new TV series and throw it on when you're bored and fighting the urge to go shopping!

5. Learn to cook!

6. Study Korean.

7. Craft something out of materials you already have laying around.

8. Plan a potluck at a friends house where you chose a country and everyone make that type of food.

9. Work out at home instead of your gym.

10. Take a run!

11. Skype someone from home. (You know your mom misses you!)

12. Do a puzzle.

13. Play Sudoku!

14. Try a crossword puzzle.

15. Learn a new card game and invite a friend over to play.

16. Meet up with some friends to watch your favorite TV show together every week. (I do this with my friend Ashley. We meet every Monday night to eat popcorn, drink coke and watch Revenge.)

17. Walk around your neighborhood and take some photos! You'll be glad you did when you finally leave this country and wanna reminisce!

18. Start a book club.

19. Volunteer at a local orphanage.

20. People watch.

21. Do an hour of yoga once in a while.

22. Read blogs. (They're pretty interesting!) wink wink

23. Learn to sew.

24. Get a part time job. (Shhh, I didn't say that!)

25. Read www.KoreaBridge.net and www.Waygook.org

26. Write a letter to someone back home and send it in the snail mail.

27. If you have a smartphone, open up an Instagram account and snap away!

28. Browse www.Reddit.com (That's Aaron's favorite.)

29. Dog sit / Cat sit for friends who need a break from their animals.

30. Clean your apartment. (You know you'll feel so much better when it's all tidy.)

31. Visit a nearby temple.

---------------------------------------------------------------------------------------------------------------------

12. Learn to cut and color your own hair!

If you're blonde like me, you know there are only a few salons in Busan that are even worth chancing, but you're still gonna pay 100,000 for your roots to be touched up and another 20,000 for a simple trim! Uugghhh. Why not learn to do it yourself? I've never been to cosmetology school, nor would I say I'm great at highlighting hair, but back in 2003, I decided that I'd rather spend that $100 a month on something other than sitting in a salon while my hair stylist painted 99 cents worth of bleach onto my hair, only to leave the salon 3 hours later with nothing but my roots touched up! I grabbed some bleach from Sally's Beauty Supply (in America) and taught myself how to highlight my own hair for $1.00 each time. Now, 10 years later, I'm still highlighting (and cutting) my hair in my own bathroom at home for about 99 cents a month! If you do the math...

---------------------------------------------------------------------------------------------------------------------

13. Don't save more than $1000 if you have debt.

---------------------------------------------------------------------------------------------------------------------

14. Pay off 1 credit card at a time.

This may sound strange, but by tackling 1 balance more than the others, it will give you a boost of instant gratification and help you feel like you're accomplishing something! Pay off your smallest debt and once it's finished tackle the next smallest debt. In other words, pay 3x, 4x, 5x's (whatever you can) of the minimum amount on 1 debt until it's gone! *** I have a friend who's working as an EPIK teacher in Korea that I've helped get on a budget in order to pay off their credit card debt and student loans. They've been able to send home about 1,600,000 a month and will have paid off almost $20,000 in 13 months! It is possible people!

---------------------------------------------------------------------------------------------------------------------

15. Open an IRA!

Once you're debt free, SAVE, SAVE, SAVE and try putting at least $100 a month in an IRA account! (If you're consistent, you'll likely end up with a million dollars by age 50! YES PLEASE! It's amazing the freedom you'll experience when you have money tucked away for a rainy day. With a bit of discipline and a lot of creativity, I've saved enough money to sustain me for a couple years in the US (just in case it takes a while for our photography business to become profitable). And it's not like I've had to sacrifice having fun while I saved it - I've traveled abroad 13 times since living here and paid for 1/2 of my wedding and honeymoon and still have money to spare. It's hard sometimes, I'm not gonna lie, but the sacrifices out weigh the end goal! Start today and make it a goal to pay off those pesky credit cards and student loan payments by the end of 2013!

---------------------------------------------------------------------------------------------------------------------

Start today!

We're 3 days away from the New Year and there's no better time to start a new years goal of being debt free, or a (₩)-millionaire, than now! And there's no better place to start than here in Korea where you're basically making $2000+ a month and have NO EXPENSES but your phone and apartment electric bill! :)

Happy New Year and may you be debt free and a (₩)-millionaire by 2014!

My personal blog - TheOtherSideOfTheMoon2009.blogspot.com

My photography blog - www.AaronNicholasPhoto.blogspot.com

Comments

Re: How to save millions while teaching in Korea!

While some of these are common sense anywhere you are, to say that here pays well is a fallacy.

People that always say pay is good here lead me to believe they have NO marketable skills at home, and thus stay here to leach of the broken and abusive system that Korea has established for the entertainment of its children.

Re: How to save millions while teaching in Korea!

thanks for posting this Jill! Any bit of encouragement helps....You have layed it out quite nicely! I will refer back to this to keep me motivated.

Re: How to save millions while teaching in Korea!

Blue1005,

I'd have to slightly disagree with you on EPIK not paying well. Let's break it down. I teach 22 (40 minute lessons) a week. I finish my classes at either 12:00pm or 12:50pm everyday and have 4 hours in the afternoon to do whatever I'd like - lesson plan (if I need too, but I usually don't because I've been teaching from the same book for 4 years) e-mail family and friends, watch TV shows, read a book, take a nap, edit photos for our photgraphy business, write blog posts, browse pinterest, etc... all while getting paid 2.9 million a month! Not to mention, I typically have at least 3 classes cancelled a week for field trips, government testing, special event days, etc. I broke it down once and I was being paid over $100 an hour for the time I was actually in the classroom! I'd say that's pretty great money, wouldn't you?!

Not to mention, 95% or so of my paycheck is ALL pocketed (The 5% being spent on my cell phone, electricty, gas, and water bill each month. No need for a car, because public transportation is great here and that excludes the need to pay for car insurance too! Oh, and health insurance is covered in EPIK's pay as well... AND PENSION too! So, yes, while I may only actually be making 34 million won a year, 32 million won of that is savings! That's $30,000 a year straight to my wallet. When's the last time you talked to someone from back home who was a teacher and had $30,000 left after paying their monthly bills?

All that to say, we get paid more than what we probably deserve to be paid.

Re: How to save millions while teaching in Korea!

Jemchu,

You're so welcome! I'm glad I could help you get, and keep, motivated! :) Good luck!

Re: How to save millions while teaching in Korea!

Absolutely agree with you Jill. It's not how much you make, it's how much you save. And in Korea (as well as China where I currently live) you can save a s*)&load!

Re: How to save millions while teaching in Korea!

some of these points are good, some are terrible.

It is ILLEGAL for you to make IRA contributions if you claim the foreign income tax exclusion. You will be slapped with hefty fines if you do this.

You should also have 3 paychecks of savings as emergency funds, not $1000. You could get fired, injuried, or have to go home unexpectedly. That plane ticket alone will wipe out your $1000.

Re: How to save millions while teaching in Korea!

What a great article!

It is excactly how I feel, except that I am a newbie to the EFL game. As a South African (with a Rand that has depreciated by around 50% in the past 4 years), the EPIK pay is even more phenomenal to us (perhaps a reason for an influx of Saffers to Korea...).

A few comments I have:

1) Don't ask me how I know this (I counted, over the desk warming boredom), your 4 million won illustration on Koreabridge is more like a 3.6 mill haha.

2) Pay in Cash: I agree with you on he psychological implications. However, I have been informed from my coteachers that at the end of your contract, you can claim tax back on purchases (I believe around 10%), but only if such purchases are done on your card. If this is the case, then I think, try get a card that has a money imprint on it, pretend that it is real money everytime you swipe (darn them money gods, I thought it was just monopoly money I was spending...)

3) Cellphones and the contracts thereof, I feel are worth an honourable mention in Korea. After arriving in my apartment, a W150 000 ($140) bill arrived, for the previous guest English teacher, who presumably 'awol'ed before paying it. I went prepaid, with 'Egsim', and while its debateably cheaper (you don't get the 'free', latest phone, or some other incentivised consumerism, it ensured that I was in control of my phone usage, and that I didnt get carried away, drunk dialing my mates in South Africa...

4) RE: algernon4 and emergency funds. While I'm not certain of American loan repayments, in SA, if you pay part of your loan of earlier, that money remains accessible from your loan, if need be. So in an emergency situation, you can re access that money.

5) Also worth honourable mention: International travel and the avoidance thereof. I've noticed, many expats in Korea find this sudden urge to become international travellers. Every holiday needs to be on the international scale. I find I massively underestimate the total cost of holidays. Over and above the flight expense, there are numerous other expesne (Visas, innoculations, permits, currency conversions fees) and then, the expense of being a 'tourist', (being ripped off, not having the local knowledge (that great cheap burger joint down the road, that only you know of) and then also needing to do supposed touristy things, that you otherwise wouldn't normally do. Visiting and more improtantly photographing the usual stereotypical, famous sights that everyone else visits, so that you can also say that you've been there too and buying some useless, overpriced souvenir to prove it. (Do you think Chinese tourists get irritated when they buy a Statue of Liberty souvenir, old to read, "made in China" on the base.")

I don't know who coined the term, Jacky Bolen makes mention a, 'staycation'; In korea in represnts a great way to see a country which has a lot to offer, and great public transportation. Staycation does need to mean staying in your aprtment. Visit a friend in Korea, or stay in a hostel. Buy yourself a tent and camp on a beach. But for your own sake, travel Korea!.

But in the case that you do choose to do an international vacation, make sure of the following: B) It is well timed. By this I mean, what is the weather like in your proposed location. What is the holiday period you've been afforded. After forking out the fixed cost for flights, ensure that they are divided over a number of days, to make it worthwhile B) It is well placed. Go to a location where your currency will boad you well. Think Vietnam, Thailand, India, Indonesia where the cheap cost of living will, atleast partially off-set the price of your flights. Avoid countries like Japan, most of Europe, or going home (Unless S Africa is your home, whereby living is cheaper, and I have free accomodation: mommy and daddy!)

All in all, thanks for the great article. Haters will hate, but at the end of the day, your frugalness is just the approach that many of these hot headed (American) youth need.